Receive CohnReznick insights and event invitations on topics relevant to your business and role.

11/11/2020

Phases in the lifecycle of a SPAC

"The roadmap to becoming a public company through a transaction with a SPAC is different when compared to a traditional IPO. What is not different is the level of preparedness required by the target company’s CFO. From accounting and reporting to risk and compliance, the CFO will need to plan adequate resources to transition from a private to a public entity." - Marisa Garcia, CPA, Partner, CohnReznick Advisory

Understanding the lifecycle of a Special Purpose Acquisition Company (SPAC) can help target company management teams appreciate the complexities and time pressure involved in completing a SPAC transaction.

Formation and Initial Public Offering (IPO)

In the formation phase, a financial sponsor (or sponsors) assembles a management team and funds an equity stake or founders stock in the SPAC. The equity investment funds initial business operations to launch an initial public offering (IPO) and identify an acquisition target. Although the ratio can vary, the founders stock often represents approximately 20% of the post-offering stock.

After selecting underwriters, the SPAC files a registration statement with the Securities and Exchange Commission (SEC) to initiate the IPO. After responding to SEC comments, the SPAC launches a road show that culminates in underwriting and the IPO, the proceeds of which are held in a trust account pending an investment opportunity. Capital is raised by issuing common stock and warrants. A warrant is a security that offers the warrant holder the right to buy or sell a security. Warrants are tradable and provide a strike price for which the stock can be purchased or sold prior to expiration.

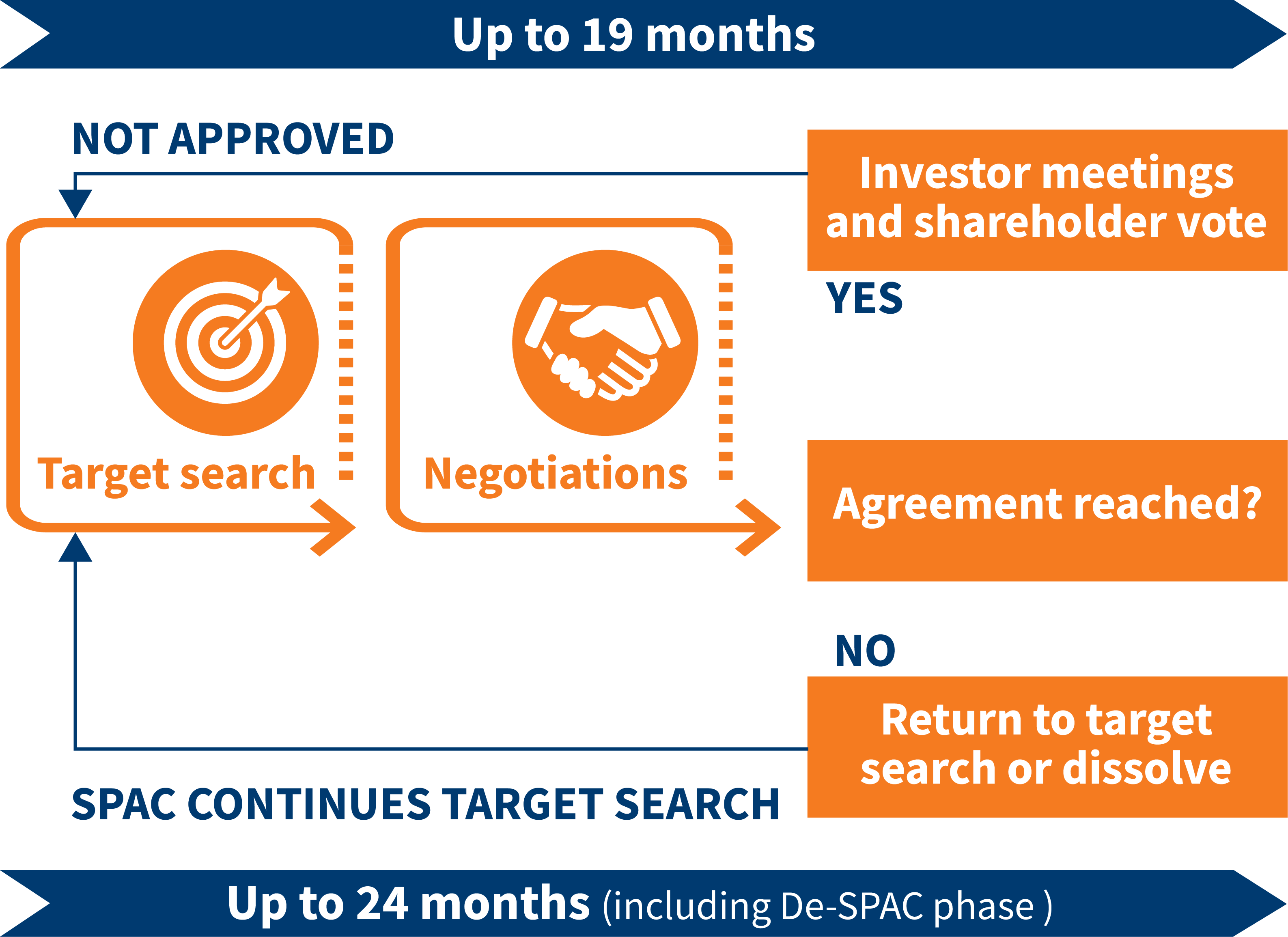

Target Search

At this point the SPAC begins its search in earnest for an acquisition target. SPACs typically have two years from the IPO date to complete an acquisition. This process proceeds in much the same way as any M&A process. The SPAC identifies and conducts due diligence on potential targets. However, because shareholders can redeem shares, the sponsors need to closely monitor cash to ensure there is sufficient funding to acquire the target and manage post-close operations. At this point, often private investment in public equity (PIPE) financing issues convertible debt, which converts to stock at the choice of the private investor, thereby diluting the equity of existing shareholders. The selection process ends with a definitive agreement between the SPAC and an acquisition target.

De-SPACing

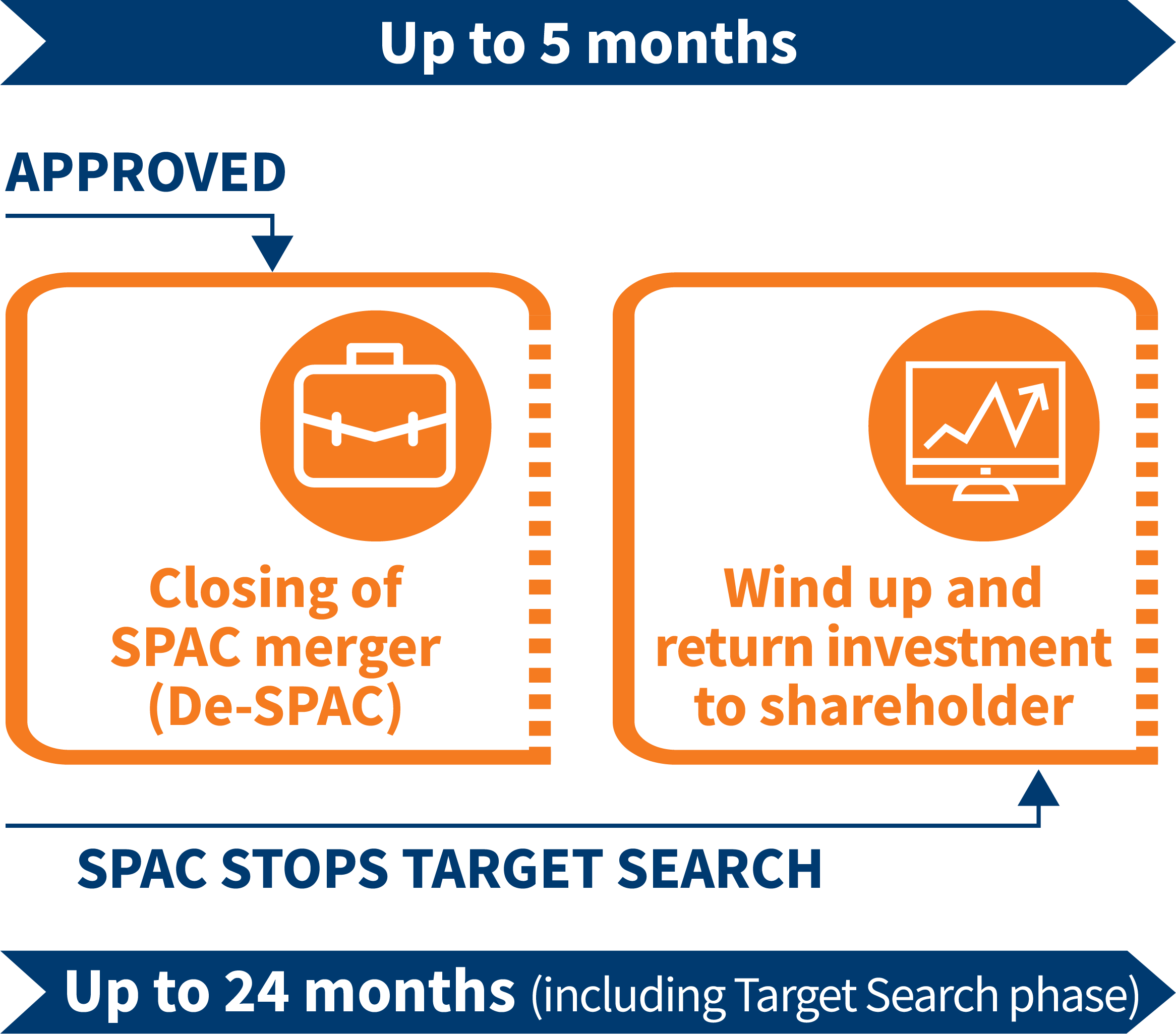

The de-SPACing process requires the buyer to obtain shareholder approval in accordance with SEC regulations. While these regulations are more complex than can be covered in detail here, typically the process includes the commitment of the founders shares to the acquisition, a redemption offer whereby SPAC shareholders can redeem their shares, and the filing of Form 8-K, which is effectively a registration statement for the transaction. It contains the information that would be filed in a Form 10, or “General Form for Registration of Securities,” which registers securities for trading in U.S. exchanges.

Managing of public company operations

At this point, the acquisition is complete and the company must comply with all public company reporting obligations under the Securities Exchange Act of 1934 and subsequent legislation. The transition is a significant one for any private company, requiring enhanced governance, controls, technology, and operating procedures.

To access the Typical 24-Month SPAC Timeline graphic in full, click below.

Contact

Claudine M. Cohen, Managing Principal, Transactions & Turnaround Advisory

646.625.5717

Cindy McLoughlin, CPA, Managing Partner, Consumer, Hospitality, and Manufacturing Industries

516.336.5510

Cindy McLoughlin

CPA, Managing Partner, Consumer, Hospitality, and Manufacturing Practice

Claudine Cohen

Managing Principal, Value360 Practice

Close

Contact

Let’s start a conversation about your company’s strategic goals and vision for the future.

Please fill all required fields*

Please verify your information and check to see if all require fields have been filled in.

SPACs: Alternative to Traditional IPO

Going Public: SPACs Offer a Capital Raising Alternative For Private Companies

Going Public as a SPAC Target Company: What to Consider and How to Prepare

Post-SPAC Transaction: Challenges and Benefits of Operating as a Public Company

This has been prepared for information purposes and general guidance only and does not constitute legal or professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is made as to the accuracy or completeness of the information contained in this publication, and CohnReznick LLP, its partners, employees and agents accept no liability, and disclaim all responsibility, for the consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.